Bull By the Horns: Fighting to save main street from Wall Street and Wall Street from Itself, Sheila Bair, 2012

Hank Ben Sheila Tim Sheila Ben

There were four central regulatory players in the great financial crisis of 2008; Ben Bernanke of the Fed, Hank Paulson of Treasury, Tim Geithner of the New York Fed and Obama’s Treasury secretary, and Sheila Bair of the FDIC. Paulson left Treasury at the end of W’s term and wrote his account of the crisis which this reader has not read. Bair left the FDIC in 2011 and this is her account. Geithner is leaving the Obama administration and will no doubt give us his account. We will have to wait for Bernanke to leave the Fed for his account.

We previously reviewed the Suskind book which featured Geithner ignoring an order from Obama to come up with a plan to break up Citigroup ( Scamming the President ). Bair recalls the meeting in question where the breakup of Citibank is discussed with the President: “Tim seemed to view his job as protecting Citigroup from me, when he should have been worried about protecting the taxpayers from Citi.” Bair says she only learned that Summers was in favor of breaking up Citigroup after reading Suskind’s book. Had she known at the time, she could have insisted that Summers arrange another meeting with the President where she could discuss and advocate using FDIC to resolve Citigroup. She never doubted this breakup could have been done.

This is the first time we learn about the “systemic risk exception” where super majorities of the Fed and FDIC boards declare that putting an institution into an FDIC type resolution would cause “systemic ramifications”. This effectively means that Treasury and the President himself must approve the resolution. Bair says of the NY Fed invoking the exception for Bear Stearns:

In fact, prior to the 2008 financial crisis, the FDIC had never invoked the systemic risk exception. But here we had the NY Fed (Geithner) going out on its own and deciding to bail out a relatively small investment bank, a perimeter player at best…I was concerned about the precedent the NY Fed was setting.

Senator Elect Elizabeth Warren

As Suskind relates, both Geithner and Summers went to great lengths to control access to Obama and the administration had an all boys club atmosphere. Christina Romer, nominal head of the Counsel of Economic Advisers, left the administration early and gets one brief mention in Bair’s account. Bair did have a close working relationship with Elizabeth Warren, newly elected Senator from Massachusetts in Ted Kennedy’s old seat, and Bair still has high hopes for the Consumer Financial Protection Bureau.

She Bear

Bair is a tough, no nonsense, plain speaking advocate of the public interest. Her fierce and protective support of the FDIC against all critics led her staff to call her “She Bear”. When she arrived at the FDIC in 2006, moral was low and the agency hadn’t closed a bank in three years. The black clouds were on the horizon and the FDIC through its own and other regulators examinations had probably the clearest picture of the looming catastrophe. She launched a major offensive to educate the public and woo the media to the role of the FDIC, the mechanisms of the bank resolution process, and reassure the public that insured bank accounts were perfectly safe.

Tim and Sheila Adversaries

Almost immediately the FDIC was overrun with bank failures; Wachovia, Countrywide, Indymac, Washington Mutual and others. She ran into her first major conflict with Geithner who wanted his client Citigroup, despite their dismal financial condition to acquire Wachovia to add their FDIC insured deposits to Citigroups small deposits. Geithner was furious when Bair continued to press Wells Fargo to purchase Wachovia, which they did without any government assistance or guarantees. Geithner doesn’t fare well in Bair’s account in this book.

Rubin’s Acolytes

Bair does a good job explaining the complex structure of financial regulation in this country. The Fed has certain regulatory functions; the FDIC domain covers any institution with insured deposits; Treasury houses two regulatory agencies, the OCC for mega banks; and the OTS for the thrifts including WAMU, Countrywide, and Golden West. While the Fed and FDIC are more independent, the Treasury is highly politicized and has been under the sway of the financial industry for some time. Citigroup’s Bob Rubin (Clinton’s first Treasury Secretary) mentored both Larry Summers and Tim Geithner and it was under Clinton that Glass-Steagall was repealed and Derivatives declared free from all regulation. And Hank Paulson was former CEO at Goldman-Sachs. The SEC and CFTC are separate and are dependent on annual budget allocations.

When Senator Dodge advocated creating a single unified regulatory agency, Bair talked him out of it because she feared a single agency would more easily fall under the control of the financial industry and become a super OCC. Besides her wars with the Citigroup dominated Geithner, Bair had continuing problems with the OCC, with John Dugan and John Walsh, comptrollers of the currency, and OTS’s John Reich, who opposed Chase’s purchase of WAMU, Reich’s last bank. The OTS is now abolished. None of these were advocating for main street and the public interest.

Reich opposed Wamu sale

Bair strongly advocated using the government through the resolution process to clean up the toxic mortgage backed securities. The FDIC successfully demonstrated simplified methods to modify mortgages en-mass during the cleanup of the thrifts. Bair was a consistent advocate for loan modification as a way to keep people in their homes and minimize the overall losses to the industry and government. She called TARP, which Paulson sold as a fund to buy toxic assets, then used it to bail out the banks and wall street with capital infusions, a case of bait and switch. She explained some of the reasons for the failure of loan modification programs. Mortgages were lumped into securities which were sold with banks providing loan servicing for low flat fees. This meant the banks were understaffed, under trained, and unsupervised. Breaking the securities into tranches meant that holders of the “safest” tranches would not be hurt financially until perhaps 20% of the mortgages defaulted so were incentivized to prefer foreclosure to restructuring loans. When robo signing was uncovered where single bank workers were fraudulently claiming to have examined the loans being foreclosed the issue moved to the front burner but no effective action resulted. Banks still had separate groups working simultaneously on foreclosure and modification of the same mortgage with customers being approved for modification at the same time they are being evicted. To this date, loan modifications are woefully inadequate and the bulk of toxic assets are still looming.

During the debate on Dodge-Frank, there was considerable discussion of FDIC style regulatory resolution verses bankruptcy. Bair uses the infamous case of the Lehman Brothers bankruptcy to prove her case that regulatory resolution is far better. Legal and other fees topped $1.5 billion and to date, creditors have recovered 21 cents on the dollar. The Lehman brand is dead and all employees lost their jobs. An FDIC style resolution results in an instant solution, preserving the brand and jobs. Her staff estimated that an FDIC resolution would have recovered 97 cents on the dollar at Lehman.

Bair is generally positive on Dodge-Frank but worries that the industry will continue to attack and modify the measures. Much of the effectiveness of Dodge-Frank will depend on the regulatory implementation and the jury is still out on much of the new complex legislation.

Bair complains that Sorkin in his book Too Big To Fail and in his columns failed to contact the FDIC to get their perspective and thus misrepresented FDIC positions and actions.

Bair spends considerable time on the Basel II accords which greatly reduced capital requirements for banks allowing the European banks to load up on sovereign debt from Greece, Italy, Spain, and Portugal. Much of the current European financial crisis is attributable directly to Basel II. Bair with a little help from the Fed was able to prevent the US from adopting Basel II. Bair then pushed Basel III to greatly increase capital requirements and to require mega banks to have even higher (9.5%) capital reserves.

Geithner Grilled after Libor Scandal Breaks

Bair notes that the Barclay misconduct in the Libor interest rate fixing scandal from mid 2005 to early 2009 took place at Barclay’s NY trading desk which was subject to Geithner’s NY Fed. The investigation was conducted jointly by the CFTC, UK authorities and the Justice Department. The investigation did not involve the NY Fed. During his appointment hearings for Treasury, Geithner proudly stated “I have never been a regulator, for better or worse.” For once he seems to have been telling the truth. Unfortunately for us, regulating was his Fed job.

Bair is very disappointed in Obama and hopes he will appoint better people in his next administration. The FDIC currently has no head. Would it be too much to hope that Obama might appoint audacious Bair to Treasury?

Going Big, FDR’s Legacy, Biden’s New Deal, and the Struggle to Save Democracy, Robert Kuttner, 2022

<>

<> <> <> <> <> <>

Economics Nobel Laureate Joseph E Stiglitz wrote the forward

The (Great) Depression should have taught us that markets are not stable and efficient–high levels of unemployment could persist for a very long time. We should not have to have had the Great Recession (2008) to relearn the lesson…We should not have had to watch the anemic recovery from the Great Recession, the result of too little fiscal policy and too much reliance on monetary policy, to have relearned that lesson.

The simplistic neoliberal ideology, which triumphed in both parties…held that downsizing government, including deregulation, privatization, and outsourcing government activities to the private sector, would lead to greater prosperity, (and)…all would benefit. Some half century later, we should declare this neoliberal experiment has been a failure, with lower growth and the benefits of that limited growth going overwhelmingly to those at the top.

Jimmy Carter, Bill Clinton, and Barack Obama each embraced neoliberal ideology to devastating effect. Biden is the first president since 1984, including Republicans that has not appointed Robert Rubin (of Goldman Sachs and Citigroup) or a protege of Rubin, like Larry Summers, to the inner circle of power.

Bill Clinton and Barack Obama took the Democratic Party deeper into the neoliberal wilderness, obsessing about budget balance, making alliances with Wall Street, and driving working-class voters into the arms of the Tea Parties and then Trump.

Stunningly, Biden jettisoned the entire set of neoliberal orthodoxies that had hobbled Democratic presidents since Jimmy Carter. Gone was the idea that deficits necessarily caused high interest rates and inflation. Gone was any illusion that we needed tax breaks for the rich in order to promote private investment. Public investment was needed at a large scale precisely because private investment had failed to serve the real economy and had enriched mainly manipulators, traders, and monopolists…It fell to Biden and his economic team to revise the globalist ideology in favor of coherent policies to rebuild American leadership in industry, technology, and supply chains, sacrificing free trade norms where necessary.

There is immense latent public support for the use of activist government to better the situation of ordinary people. Foreign policy adventures, such as Vietnam, Iraq, and Afghanistan, can serve as distractions from domestics issues that play to Democratic strength, and can wreck the unity of the coalition needed to pursue domestic progressivism. So, obviously, can racism and continuing legacy of slavery and segregation. But the big challenge is political economy.

Biden needs to go beyond what even FDR achieved in containing a corrupted capitalist system, because that system today is the wellspring of so much policy failure, and so much political and economic inequality, as well as the corruption of too many Democratic leaders, all of which kindles support for Trumpism.

<> <> <> <> <> <> <>

In the standard Roosevelt narrative, FDR restores hope. And he then goes about restoring the economy, using powers of government to put people back to work, and devising new public entities to accomplish what the private sector had bungled. He increases the prestige of the public sector and public solutions. He uses public deficits to restore purchasing power. He virtually invents a national system of social insurance with the Social Security Act. He puts government on the side of worker’s right to organize with the Wagner Act, and then regulates wages and hours directly with the 1938 Fair Labor Standards Act.

Ordinarily, the Treasury Department is the home of the most conservative officials of an administration. Democratic presidents, seeking to reassure financial markets typically place Wall Street veterans at the Treasury. This was the practice of Johnson, Carter, Clinton, and Obama. But the Roosevelt Treasury was the home of radicals. The most radical was Harry Dexter White, the top U.S. government architect of the postwar global financial system. White was a close collaborator of the the chairman of Bretton Woods conference, John Maynard Keynes.

The Democratic defensive unease on national security policy combined with the unfinished business of racial justice to destroy Johnson’s presidency. The Vietnam debacle also shattered the New Deal coalition and the hopes of progressive Democrats for half a century.

As the Obama administration and the Fed did the bidding of the biggest banks, (Elizabeth) Warren and the oversight panel would become one of two sources of loyal opposition, calling for a far more radical, Rooseveltian approach. The other was the FDIC, which was the last regulatory hawk in laissez-faire Washington, because its trust fund had to be tapped to pay depositors when an insured bank failed. The chair of the FDIC was a tough and savvy regulator named Sheila Bair…The financial collapse should have set up Obama to orchestrate a resurrection the the New Deal–the containment of the toxic tendencies of private finance, the expansion of government to do what markets could not, and the use of the crisis as an object lesson…Most of what he did propped up the banking system rather than cleaning it out or seriously re-regulating finance. Obama’s obsession with deficit reduction made the recovery far too slow.

The serial forms of deregulation that finally crashed the economy in September 2008 had been building and accumulating for several decades. Three earlier crashes, harbinger of the general collapse of 2008, had been contained because the degree of leverage, opacity, conflicts of interest, deregulation, non-supervision, and above all interpenetration had not quit reached the level of the early 2000s. But each was a clear warning that went unheeded.

The 1990s S&L collapse saw the conviction of more than a thousand executives. The Crash of hedge fund Long Term Capital Management in 1998 led to no reforms. The dot-com and energy crash of 2000 also led to no reform.

Kuttner spends some time on the explosion of private equity and the toxic effect on nursing homes, newspapers creating “news desserts” throughout the country, and retail.

Kuttner also talks about the the collateralized loan obligation CLO that have replaced the discredited CDO behind the 2008 crash The US market for CLOs excedes $850 billion in 2022.

If the New Deal proposition is that government can be effective in solving problems and helping ordinary people, climate change makes that harder to pull off, because worsened climate events are baked in for years to come. Even if Biden does everything right, the everyday experience of extreme climate events will intensify.

Kuttner concludes with a discussion of the importance of the upcoming 2022 midterm elections. Only three Presidents over the last 100 years have seen their party increase its control of both houses of congress in the midterm elections; Roosevelt in 1934 because of the popularity of his programs; Clinton in 1998 because the Republicans overreached in trying to impeach him; and George W. Bush in 2002 because of the shock of the 9/11 attacks. Can Bidden become the fourth in 2022?

Capital and Ideology, Thomas Piketty, 2020

<> <> <> <> <>

A continuation of Piketty’s earlier 2014 work extending his previous analysis starting from 1500 to the present and adding France, India, China, Germany, Spain. the Nordic countries, Russia and Eastern Europe, the Petro-Monarchies, etc.

<>

Today, the postcommunist societies of Russia, China, and to a certain extent Eastern Europe…have become hypercapitalism’s staunchest allies. This is a direct consequence of the disaster of Socialism and Marxism and the consequence of all egalitarian internationalist ambitions. So great was the communist disaster that it overshadowed even the damage done by the ideologies of slavery, colonialism, and racialism and obscured the ties between those ideologies and the ideology of ownership and hypercapitalism–no mean feat.

Furthermore, social democrats never really reconsidered the issue of just ownership after the collapse of communism. The postwar social-democratic compromise was built in haste, and issues such as progressive taxation, temporary ownership, circulation of ownership (for example, by means of a universal capital grant financed by a progressive tax on property and inheritances), power sharing in firms (via co-management or self management), democratic budgeting and public ownership were never explored as fully or systematically as they might have been.

It (modern property law) originated…with Christian doctrine, which sought over many centuries to secure the property rights of the Church as both a religious and a property-owning organization.

…the concentration of private property, which was already extremely high in 1800-1810, only slightly lower than on the eve of the (French) Revolution, steadily increased throughout the nineteenth century and up to the eve of World War I…The case of Paris is especially noteworthy; there, the wealthiest 1 percent owned nearly 50 percent of all property in 1800-1810 and more than 65 percent on the eve of World War I.

As for achieving real equality, however, the great promise of the (French) Revolution went unfulfilled…And when a progressive income tax was finally adoption on July 15, 1914, it was not to finance schools or public services but to pay for war with Germany.

<> <> <> <> <>

When slavery was abolished in the 19th Century, the discussion in slave owning nations concerned compensation for the owner’s of slaves, never about compensation for the slaves.

It is easy to see that in a society where slaves represented virtually the entire work force, their market value could reach astronomical levels, potentially as high as seven or eight years of annual production…Recall that France saddled Haiti with a debt equivalent to three years of Haitian nation income in 1825 yet remained convinced that it was making sacrifices compared to what slaves in Saint-Dominique actually yielded in profit.

In 1860, the market value of (US) slaves (4 million in number) exceeded 250 percent of the annual income of the southern states and came close to 100 percent of the annual income of all the states. If compensation had been paid, it would have been saddled with interest and principal payments for decades.

The secession of the southern states and the resulting Civil War ended these discussions and US slave owners were never compensated for their loss of property as a result of the war and the emancipation proclamation.

Piketty follows the transformation, starting around 1500, of society from Ternary (Clergy, Nobility, Third estate–the workers) to Ownership societies with a centralized state. This transformation was accompanied by the rapid development of arms, warships, and navigation, needed to support the endless wars among the new nation states. This technological development of war tools enabled the co development of slavery and colonialism. Even the Ottoman and Chinese Empires were no match for the modern war machine. Gunboat diplomacy reigned supreme into the twentieth century. An extreme example are the two opium wars of Britain against China in the mid nineteenth century. Not only did China have to allow the sale of opium in China, but China was saddled with massive reparations for the costs of the wars.

Japanese Depiction of Perry’s black ships

<> <>

Japan reacted to the American (Admiral Perry), French and British visit by warship in the mid nineteenth century with the Meiji reformation, whereby Japan acquired and built its own advanced arms and warships and became a colonial power in its own right.

In the period 1880-1914, the United Kingdom and France earned so much from their investments in the rest of the world (roughly 5 percent additional national income for France and more than 8 percent for the United Kingdom) that they could allow themselves to run persistent structural trade deficits (an average of 1-2 percent of national income for both countries) while continuing to accumulate claims on the rest of the world at an accelerated pace. In other words, the rest of the world labored to increase consumption and standard of living of the colonial powers, even as it became increasingly indebted to those powers.

On Colonial state tax revenues in the eighteenth century:

…both countries (England and France) were taking in 600-900 tons of silver in 1700, 800-1100 tons in the 1750’s, and 1600-1900 tons in the 1780’s, leaving all other European powers far behind. Importantly, Ottoman tax receipts remained virtually unchanged from 1500 to 1780; barely 150-200 tons. After 1750, it was not only France and England that had a far greater tax capacity than the Ottoman Empire; so did Austria, Prussia, Spain, and Holland.

…the development of the modern state involved two great leaps forward. The first unfolded between 1500 and 1800 in the leading states of Europe, which were able to increase their tax revenues from barely 1-2 percent of national income to about 6-8 percent. This process was accompanied by the development of ownership societies at home and colonial empires abroad. The second leap forward came in the period 1930-1980, when the rich countries as a group went from tax revenues of 8-10 percent of national income on the eve of World War I to revenues of 30-50 percent of national income in the 1980s. This transformation was accompanied by a broad process of economic development and historic improvement in living conditions and gave rise to various forms of social-democratic society…It proved difficult to extend the second leap forward to poorer countries in the late twentieth and early twenty-first centuries…

If we include all military conflicts across the continent in each period, we find that European countries were at war 95 percent in the sixteenth centry, 94 percent in the seventeenth century, and still 78 percent in the eighteenth century (compared to 40 percent in the nineteenth century and 54 percent in the twentieth century). The period 1500-1800 was one of incessant rivalry among Europe’s military powers, and this is what fueled the development of unprecedented fiscal capacity as well as numerous technological innovations, particularly in the areas of artillery and warships.

By the end of the American Revolutionary and Napoleonic Wars (1792-1815), British public debt had soared to more than 200 percent of national income, the debt was so high that one-third of the taxes paid by British taxpayers between 1815 and 1914 (mainly by people of middle and low income) was devoted to repayment of the debt and interest (profiting the wealthy who had lent the government money to pay for the wars)…It also might have been preferable to tax the wealthy rather than allow them to become still wealthier by buying government bonds…with political power in the hands of the wealthy, the choice was made to spend money on the military and to finance it with public debt, and this helped to secure European domination over the rest of the world.

…these protectionist and mercantilist measures, imposed on the the rest of the world at gunpoint, played a significant role in achieving British and European industrial domination. According to available estimates, the Chinese and Indian share of global manufacturing output, which was still 53 percent in 1800, had fallen to 5 percent by 1900.

The colonial ideology that seeks to liberate and civilize nations in spite of themselves generally leads to disaster, no matter what the color of the colonizer’s skin (Japan).

The success of Japan’s proprietarian and industrial transition shows that the mechanisms at work have nothing whatsoever to do with Christian culture or Eueopean civilization…the Japanese experiences shows that proactive policies, especially regarding public infrastructure and investments in education, can overcome very strong and longstanding status inequalities in a matter of decades…we will see that the reduction of social inequality in Japan was further assisted by an ambitious program of agrarian reform in the period 1945-1950 as well as by highly progressive taxation of top incomes and large estates.

The fall of ownership society in the period 1914-1945 can be analyzed as a consequence of three challenges; the challenge of inequality with European ownership societies, which led to the emergence first of counterdiscourses and then of communist and social-democratic counter-regimes in the late nineteenth and first half of the twentieth centuries; the challenge of inequality among countries, which led to critiques of the colonial order and the rise of increasingly powerful independence movements in the same period; and finally a nationalist and identitarian challenge, which heightened competition among the European powers and eventually led to their self-destruction through war and genocide in the period 1914-1945.

The period from 1726-1914 saw low inflation and complete stability in the value of the pound sterling and the French gold franc. World War I put an end to monetary stability and the suspension of convertibility of their currencies into silver or gold.

…from 1914 to 1950 inflation averaged 13 percent a year in France (equivalent to a hundred fold increase in the price level) and 17 percent in Germany (a three hundredfold price increase).

…ownership societies that seemed so prosperous and solid on the eve of World War I collapsed between 1914-and 1945. The collapse was so complete that nominally capitalist countries actually turned into social democracies between 1950 and 1980 through a mixture of policies including nationalizations, public education, health and pension reforms, and progressive taxation of the highest incomes and largest fortunes. Despite undeniable success, however, these social-democratic societies began to run into trouble in the 1980’s. Specifically, they proved unable to cope with rampant inequality that began to develop more of less everywhere around that time.

Why did social democratic societies fail after 1980?

Ronald Reagan (R) and Margaret Thatcher wave after their arrival in Camp David, 22 december 1984, before their meeting. (Photo credit should read ARCHIVES UPI/AFP/Getty Images)

In the first place, attempts to institute new forms of power sharing and social ownership of firms remained confined to a small number of countries (especially German and Sweden). This avenue of reform was never explored fully as it might have been, even though it offered one of the most promising responses to the challenge of transcending private property and capitalism. Second, social democracy did not have a good answer to one pressing question; how to provide equal access to education and knowledge, particularly higher education. Finally, we will look at social-democratic thinking about taxation, especially progressive taxation of wealth. Social democracy did not succeed in building new transnational federal forms of shared sovereignty or social and fiscal justice. Today’s globalized economy is one in which regulation in all its forms has been undermined by free trade and free circulation of capital, instituted by agreements to which social democrats consented or even instigated. In any case, they had no alternative to offer. The resulting heightened international competition has gravely endangered the social contract (and consent to taxation) on which the social-democratic states of the twentieth century were built.

The French and British never embraced corporate power sharing and social ownership preferring nationalization of private companies:

Then in 1986-1988 the Gaullist and liberal parties returned to power in a new context of privatization and deregulation under Thatcher and Reagan, while at the the same time the Communist bloc was slowly crumbling. This led to the privatization of most of the companies that had been nationalized between 1945-1982.

…from 1917 to 1991, new thinking about private property was blocked by the bipolar opposition of Soviet Communism and American capitalism. One was either for unlimited state ownership or for full private shareholder ownership….The fall of the Soviet Union inaugurated a new period of unlimited faith in private property from which we have not yet completely emerged but which is beginning to show serious signs of exhaustion.

On the massive inequality that developed in the United States from about 1980:

The bottom 50 percent of the income distribution claimed about 20 percent of national income from 1960 to 1980, but that share has been divided in half, falling to just 12 percent in 2010-2015. The top centile’s share has moved in the opposite direction, from barely 11 percent to more than 20 percent…the share of total income going to the bottom 50 percent in Europe remains significantly larger than the share going to the top centile.

To sum up: in the light of the history of the past two centuries, educational equality played a more important sole in economic development than the sacrilization of inequality, property, and stability. More generally, history demonstrated the recurrent risk of an “inequality trap” which many societies have faced throughout the ages. Elite discourse tends to overvalue stability, and especially the perpetuation of existing property rights, whereas development often requires a redefinition of property relations and opening up of opportunities to new groups.

On the failures of progressive taxation:

First, parties of the left failed to foster the kind of international cooperation needed to protect and extend progressive taxation; indeed at times they contributed to the fiscal competition that has proved devastating to the very idea of fiscal justice. Second, thinking about just taxation too often neglected the idea of a progressive wealth tax, despite its importance for any ambitious attempt to transcend private capitalism, particularly if used to finance a universal capital endowment and promote greater circulation of wealth.

…we now know that the top centile’s share of total wealth can fall from 70 percent to 20 percent without impeding growth (quite the contrary, as Western European experience in the twentieth century shows). We know from experience with Germanic and Nordic versions of co-management that employee and shareholder representatives can each control half the voting rights in a firm and that such power sharing can improve overall economic performance.

On tax havens:

…this minimum estimate implies that the financial assets tucked away in tax havens are roughly equal to the total amount of all financial assets legal owned by Russian households inside Russia (roughly one year of national income). In other words, off shore property has become at least as important in macroeconomic terms as legal financial property…In a sense, illegality has become the norm.

…by exploiting data made public by the Bank for International Settlements (BIS) and the Swiss National Bank (SNB) on countries where assets are held, one can estimate each country’s approximate share of offshore assets held in tax havens relative to the total (lawful and unlawful) assets held by residents of each country. The results are as follows; “only” 4 percent for the United States, 10 percent for Europe, 22 percent for Latin America, 30 percent for Africa, 50 percent for Russia, and 57 percent for the petroleum monarchies.

On China:

China thus appears to have settled on a mixed-economy property structure: the country is no longer communist since nearly 70 percent of all property is now private, but it is not completely capitalist either because public property still accounts for a little more than 30 percent of the total–a minority share but still substantial. Because the Chinese government, led by the CCP, owns a third of all there is to own in the country, its scope for economic intervention is large: it can decide where to invest, create jobs, and launch regional development programs.

If we compare China to the other Asian giant, India, it is clear that since the early 1980s China has been both more efficient in terms of growth and more egualitarian in terms of income distribution (or, rather, less inegalitarian, in the sense that concentration of income has increased less dramatically than in India)…one reason for this difference is that China has been able to invest more in public infrastructure, education, and health care. China achieved a much higher level of tax revenue than India, where basic health-care and educational services remain notoriously underfinanced. China has nearly matched Western levels of taxation, taking in roughly 30 percent of national income in taxes (and roughly 40 percent if one includes profits from public firms and sale of public lands).

On the dangers posed by the central banks:

After the bankruptcy of Lehman Brothers in September 2008 and the ensuing financial panic, things changed completely…The world’s major central banks devised increasingly complex money-creation schemes collectively described by the enigmatic term “quantitative easing” (QE). In concrete terms, QE involves lending to the banking sectors for longer and longer periods (three months, six months, or even a year rather than a few days or weeks) and buying bonds issued by private firms and governments with even longer duration (of several years) and in much greater quantities than before. The Federal Reserve was the first to react In September 2008 its balance sheet increased from the equivalent of 5 percent of GDP to 15 percent; in other words the Fed created money equivalent to 10 percent of US GDP in a few weeks time. This proactive stance would continue in subsequent years; the Fed’s balance sheet had risen to 25 percent of GDP by the end of 2014…In Europe the reaction was slower. The ECB and other European authorities took longer to understand that massive intervention by the central bank was the only way to stabilize financial markets and reduce the “spread” between the interest rates of the various European countries. Since then, the ECB purchases of public and private bonds have accelerated, however, and the ECB’s balance sheet stood at 40 percent of Eurozone GDP at the end of 2018…By avoiding cascading bank failures and acting as “lender of last resort”, the Fed and ECB did not repeat the errors that the central banks committed in the interwar years, when orthodox “liquidationist” thinking (based on the idea that bad banks must be allowed to fail so that the economy can restart) helped push the world over the edge of the the abyss…What makes central banks so powerful is their ability to act extremely rapidly.

Piketty does not discuss the New Deal US Federal Deposit Insurance Corporation FDIC program which allows the federal government to instantly take over failing banks, reorganize them with new management, and reopen them after a single weekend, assuring depositors that their savings are insured and immediately available. Obama and his treasury secretary Tim Geithner refused to allow the Shiela Bair led FDIC to break up and reorganize the failing banks during the 2008 crisis. This would have been the available and desired solution to the failures.

…the danger is that these monetary policies, by avoiding the worst gave the impression that no broader structural change in social, fiscal, or economic policy was necessary. Nevertheless, the fact is that central banks are not equipped to solve all the world’s problems or to serve as the ultimate regulator of the capitalist system…To combat excessive financial deregulation, rising inequality, and climate change, other public institutions are necessary; laws, taxes, and treaties drafted by parliaments relying on collective deliberation and democratic procedures.

In the abstract, there is nothing to stop central banks from enlarging their balance sheets by a factor of ten or even more…From a strickly technical standpoint, the Fed or ECB could create dollars or euros worth 600 percent of GDP and attempt to buy all the private wealth of the United States or Western Europe…central banks and their boards of governors are no better equipped to administer all of a country’s property than were the Soviet Union’s central planners.

…the Bank of Japan and Swiss National Bank both have balance sheets in excess of 100 percent of GDP…It is nevertheless impossible to rule out that similar things will someday happen to the Eurozone or the United States. Financial globalization has assumed such proportions that it may lead those responsible for setting monetary policy step by step toward decisions that would have been unthinkable only a few years before.

Many citizens have quite understandably begun to ask why such sums were created to bail out financial institutions, with little apparent effect in jump-starting the European economy, and why it shouldn’t be possible to mobilize similar resource to help struggling workers, develop public infrastructure, or finance large investments in renewable sources of energy. Indeed it would be by no means absurd for European governments to borrow at current low interest rates to finance useful investments, on two conditions; first, such investments should be decided democratically, in parliament with open debate, and not by a Governing Council meeting behind closed doors; and second, it would be dangerous to lend credence to the notion that every problem can be resolved by printing money and taking on debt. The principal instrument for mobilizing resources to undertake common political projects was and remains taxation, democratically decided and levied on the base of each taxpayer’s economic resources and ability to pay, in total transparency.

And yet the Democratic presidents who followed Reagan, Bill Clinton (1992-2000) and Barack Obama (2008-2016) never made any real attempt to revise the narrative or reverse the policies of the 1980s. In particular, in regard to the reduction of the progressive income tax (whose top marginal rate fell to an average of 39 percent from 1980 to 2018, half its level in the period 1932-1980) and the de-indexing of the federal minimum wage (which led to a clear loss of purchasing power since 1980), the Clinton and Obama administrations basically validated and perpetuated the basic thrust of policy under Reagan…But it may also be that acceptance of the new fiscal and social agenda was partly due to the transformation of the Democratic electorate and to a political and strategic choice to rely more heavily on the party’s new and highly educated supporters, who may have found the turn toward less redistributive policies personally advantageous.

In particular, higher-income voters voted more heavily for Tony Blair’s New Labour in the period 1997-2005 than they had voted for Labour previously. That may seem logical given that New Labour also attracted more and more votes among college-educated people and its fiscal policies were relatively favorable to high earners. Just as the Clinton (1992-2000) and Obama (2008-2016) administrations had validated and perpetuated the Reagan reforms of the 1980s, New Labour governments in the period 1997-2010 largely validated and perpetuated the fiscal reforms of the Thatcher era.

I have tried to highlight the significant dangers posed by the rise of socioeconomic inequality since 1980. In a period marked by internationalization of trade and rapid expansion of higher education, social-democratic parties failed to adapt quickly enough, and the left-right cleavage that had made possible the mid-twentieth-century reduction of inequality gradually fell apart. The conservative revolution of the 1980s, the collapse of Soviet communism, and the development of neo-proprietarian ideology vastly increased the concentration of income and wealth in the first two decades of the twenty first century. For want of a constructive egalitarian and universal political outlet, these tensions have fostered the kinds of nationalist identity cleavages that we see today in practically every part of the world…When people are told that there is no credible alternative to the socioeconomic organization and class inequality that exists today, it is not surprising that they invest their hopes in defending their borders and identities instead.

In the broadest terms, the tax system of the just society would rest on three principal progressive taxes: a progressive annual tax on property, a progressive tax on inheritances, and a progressive tax on income. As indicated here, the annual property tax and the inheritance tax would together yield about 5 percent of national income, all of which would be used to finance capital endowments. The progressive income tax, would yield about 45 percent of national income, which would be used to finance all other public expenditures, including the basic income and, above all, the welfare state (which would cover health, education, pensions, and so on).

The model of participatory socialism proposed here rests on two key pillars; first, social ownership and shared voting rights in firms, and second, temporary ownership and circulation of capital. These are the essential tools for transcending the current system of private ownership. By combining them, we can achieve a system of ownership that has little in common with today’s private capitalism; indeed it amounts to a a genuine transcendence of capitalism.

If every individual is to have a chance of finding decently remunerated employment, we must put an end to the hypocritical practice of investing more in elitist educational programs and institutions than in institutions that cater to the disadvantaged. The labor code and, more generally the entire legal system need to be overhauled. New systems of wage bargaining, a higher minimum wage, a fairer wage scale, and sharing of voting rights within firms between workers and shareholders can all contribute to the establishment of a just wage, a more equal distribution of economic power, and a deeper involvement of workers in shaping the strategy of their employers.

The central goal of democratic equality vouchers is to promote participatory and egalitarian democracy. Currently, the prevalence of private (political) financing significantly biases the political process. This is particularly true of the United States where campaign finance laws (always inadequate) have been set aside by recent decisions of the Supreme Court. But it is also true in emerging democracies such as India and Brazil as well as in Europe, where current laws are equally inadequate and in some cases totally scandalous.

The redefinition of the global legal framework will require abandonment of some existing treaties, most notably those concerning the free circulation of capital that came into effect in the 1980s-1990s because these stand in the way of meeting the above mentioned goals. These treaties will need to be replaced by new rules based on the principles of financial transparency, fiscal cooperation, and transnational democracy.

Finally it should be noted that this book was written before the start of the global covid19 pandemic and the global recession/depression. Undoubtedly much is about to change socially and politically in response.

Homewreckers; How a Gang of Wall Street Kingpins, Hedge Fund Magnates, Crooked Banks, and Vulture Capitalists Suckered Millions Out of Their Homes and Demolished the American Dream, Aaron Glantz, 2019

Steve Mnuchin, Poster Child of the Homewreckers

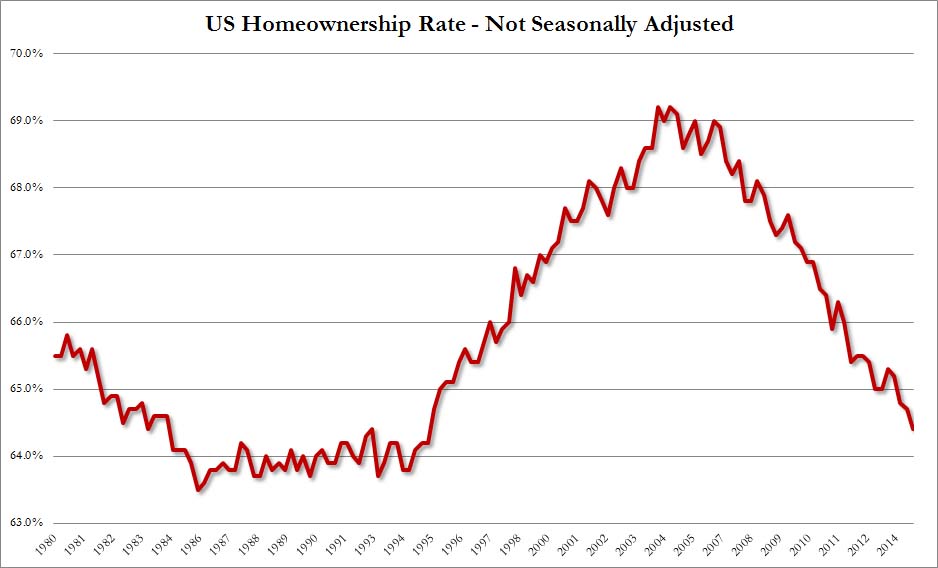

10 million Americans lost their homes as a result of the Financial Crisis of 2007-2008. By 2010 more than 10% of Americans were unemployed. The Financial Crisis left 45 more million Americans below the poverty line. This book focuses on a handful of predators whose actions would not have been possible without the full cooperation and assistance of the Federal government and the Obama administration. Most of those houses became rentals owned by a handful of huge LLC limited partnerships. The new owners of all these houses are holding them waiting for real estate prices to recover sufficiently to satisfy their greedy requirements to profit from a disaster. These houses are not available to individual home buyers which is artificially driving the prices of homes higher. Charts (not shown in this book) illustrate the changes.

The financial crisis of 2007-2008 was the direct result of a Federal government failure of regulation of the banking industry and the confusion of FDIC banking with Wall Street style speculation. Three critical changes were required to assure it didn’t happen again: 1) Reestablish the Glass-Steagall Act to again separate FDIC regulated banking from Wall Street Speculation. This act was passed in 1933 and repealed in 1999 under Clinton. 2) Severely Regulate or outlaw financial derivatives, created by the Commodity Futures Modernization Act of 2000 signed into law by Clinton. 3) Break up the big banks and separate their FDIC insured portions from their Wall Street operations. Since all banks were insolvent by 2008, the FDIC had full authority to take over all banks, remove all management, and do whatever was necessary to restore sound banking practice. See also Sheila Bair’s book. The Obama administration did none of these things. These three changes were necessary and possible but re regulation would have required even more changes before banking could return to its rightful boring self. The blame for what happened to those 10 million American families who lost their homes couldn’t be clearer. Clinton broke banking and Obama didn’t fix it even though he could have. Now this book;

Through all of this, the administration of Barack Obama, like George W. Bush’s before him, did very little to stem the tide of foreclosures. …Congress passed a massive bank bailout that did little to help individual borrowers. The terms of the deals the federal government brokered afterward, like the sale of IndyMac to Steve Mnuchin’s group of hedge fund managers, encouraged foreclosures.

Then, as foreclosures spiraled out of control and the number of vacant and foreclosed homes mounted, the federal government did almost nothing to prevent communities from collapsing entirely…The Neighborhood Stabilization Program, extended grants to hard-hit communities to provide “emergency assistance to stabilize communities with high rates of abandoned and foreclosed homes.” …A typical NSP grant went to Riverside, California, where fourteen thousand homes were lost to foreclosure… The city…received just $6.5 million–barely enough to buy fifty homes (not even 1 percent of Riverside’s foreclosures).

The Barracks

The Depression era HOLC, by contrast, acquired nearly two hundred thousand properties through foreclosure. 90 percent of those home were sold to families. The Obama Federal Housing Finance Agency, which oversees Fannie Mae and Freddie Mac, simply bundled foreclosed houses into blocks sized between 500 and 10,000 homes at a time to be sold to the Federally subsidized (bailed out) banks and eventually to vulture LLCs. The banks had no intention of finding individual buyers and issuing mortgages so all these homes so they unloaded then in bulk to the vulture LLCs. No attempt was made to determine if the buyers were qualified to manage these properties. There were no promises by buyers to maintain the properties, keep rents affordable, or engage with the community. The home were simply dumped by the government and the banks. And house prices kept dropping through 2012. Las Vegas, Phoenix, Spokane, Riverside and San Bernadino County saw prices drop more than 50 percent. By late 2011 the fire sale was on. The book features Tom Barrack whose source of money to make the home purchases is murky but involves the Cayman Islands and strong suspicions of money laundering and tax evasion. It all ends with Delaware (Biden) LLCs and ultimately to Barrack’s parent company, Colony Capital LLC. Colony eventually amassed an empire of 31,000 houses, rivaling the size of Blackstone’s house empire. Chase lent Colony $1.1 Billion for 7,563 homes. This giant bundle created a derivative that was carved up into tranches and sold on the bond market. But the two LLC predatory vulture groups featured in this book taken together total about 60,000 houses which represent about .6 percent of the 10 million houses lost. Where are the rest of those 10 million houses?

The book outlines the takeover of two failed banks, BankUnited of Florida, and IndyMac of California. Both deals were very costly for the government and resulted in private equity LLC ownership by wealth seeking individuals without a shred of empathy for who was hurt by their actions. The preditors see themselves as simply taking advantage of market opportunities presented by the federal government.

Attention is also given to the unloading of OneWest bank to a who’s who of investors for $1.6 billion. The deal left the government on the hook for any losses incurred in dumping the bank’s mortgages. When the new owners stripped and sold the bank, their return was $5 billion tripling their investment in less than 5 years. The investors included George Soros, John Thain, John Paulson, J.C. Flowers, and others.

Sandy Jolley Reverse Mortgage Whistle blower

Drawing special attention here is the reverse mortgage for the elderly, pioneered during the Reagan years but kept small by government rules. By 2006, the cap was raised to 275,000. Even the government was selling them and packaging its own fully guaranteed reverse mortgages into mortgage backed securities, sold and sliced by the same speculators that brought down the whole system. Most troubling, subprime specialists like IndyMac started selling reverse mortgages using “boiler room” sales tactics and preying on seniors lacking the mental capacity to understand the contracts they signed. Glantz features one deal involving an elderley wife with Alzheimer’s and a dying husband unable to understand the reverse mortgage he was agreeing to. When the husband died, the daughter Sandy Jolley moved back home to care for her mother and fight off foreclosure. In any system with a functioning justice system, the reverse mortgage contracts would have been vacated, the home restored, and damages assessed. None of this happened but Jolley kept fighting, assembling a large group of similarly displaced homeowners and becoming a federal whistle blower. Twelve years after her parent’s reverse mortgage was signed, the case was settled in 2017 with a typical slap on the wrist award and no admission of wrongdoing. Sandy Jolley’s whistle blower’s reward was $978,000.

Too big to fail ($50 billion plus in assets enshrined under Dodd-Frank now raised to $250 billion) Chase bank acquired Bear Sterns and Washington Mutual Bank in 2008. Wells Fargo acquired Wachovia Bank in 2008. Bank of America acquired Merrill Lynch in 2008. All banks accelerated their foreclosure and bundled them for sale to vulture capital LLCs as the easiest way to get the houses off their books, and the Obama government was guaranteeing any losses incurred. All banks greatly decreased their mortgage business and offered mortgages only to customers with high income and impeccable credit. From 2014 to 2016 Chase issued six thousand mortgages under the FHA program (usually used by first time buyers). During this same period Chase loaned Tom Barrack’s Colony $3.3 billion as it created six mortgage backed securities covering 23,000 homes. For first time home buyers an entire generation has had no reasonably priced starter homes and no way to buy the few that were out there. Yet the Federal Reserve held interest rates at near zero throughout the period. Practically, this has meant FDIC deposits are practically free for banks and cheap money was available for speculation and vulture purposes.

The Vulture LLCs that acquired all these houses, bundled them into large groups and securitized them using the same vehicles journalists were calling weapons of mass destruction in 2008. The bundles were diced into trenches to receive different ratings by the same agencies like Moodies who contributed to the 2008 collapse. Typically 80 percent of the bundles received AAA ratings. Glantz researched a tiny Los Angeles Home which listed a mysterious LLC as owner and a lien for $500 million (later refinanced for $900 million).

When housing prices reach a suitably high level, no doubt the LLCs will start selling their huge collections of houses but for the time being they can continue to collect ever increasing rents while spending a minimum on maintenance. Expect these houses to be in awful shape when they eventually reenter the housing market as single family homes.

An article in RCLCO real estate advisors in 2016 found that the seven largest LLCs owned and rented out a total of 170,000 single family houses. A chart in this article shows that single family rental units now comprise 35 percent of total rentals. If there are 43 million renters, then 15 million would be renting single family units. The 10 million foreclosed homes must represent a very sizable portion of these rentals. The article puts the increase in occupied single family rentals during the period 2005-2014 at 3.8 million (probably under estimated) while the increase in single family ownership increased by just a tiny 482,000. It appears the government does little to actually track statistically what happened to foreclosed houses or to track what the deals assuring that banks or LLCs wouldn’t lose money from foreclosures actually cost the government. Mother Jones in 2009 put the financial crisis federal bailout cost at a staggering $14.4 trillion. At present, we seem to have no accurate way to determine what happened to the bulk of those 10 million foreclosed houses. The $14 trillion figure also appears in Ron Suskind’s 2011 Book.

Many of the vultures moved to the Trump administration and the administration’s big tax reduction giveaway showered particular largess on corporations and LLCs.

The Age of Surveillance Capitalism; The Fight for a Human Future at the New Frontier of Power, Shoshana Zuboff, 2018

This is a look at the transformation of Google, Facebook, and others from their initial mission to serve their users to the exploitation of those users by selling their privacy to the highest bidder to achieve enormous personal wealth and power.

In her personal experience Zuboff describes sitting as a nineteen year old in the back of a seminar where Thomas Friedman (founder of the Chicago school of economics) instructs doctoral students who will soon run the economy of Chile after the CIA inspired coup and assassination of elected President Salvador Allende in favor of the Pinochet military dictatorship in 1973.

Thomas Friedman and Friedrich Hayek, economics as ideology and their opposite John Maynard Keynes

Zuboff also briefly alludes to debates she had at Harvard with the aging and discredited behaviorist BF Skinner, author of the novel Walden Two. She spends time in the book discussing Alex Pentland of the MIT media lab who she considers a BF Skinner intellectual successor armed with the tools Skinner could only dream of having and using. She calls Pentland a high priest of Surveillance capitalism. Pentland helps provide the intellectual justification that legitimizes instrumentarian (a new word coined by Zuboff) practices. Pentland never mentions Skinner in his work but his behavior modification goals are the same.

BF Skinner at Harvard and Alex Pentland of MIT Media Lab

Zuboff explains why user consent through opt-in or opt-out has been rendered meaningless under Surveillance Capitalism. To read a single contract agreement in detail might take hours and with third parties almost always involved there may be 1,000 individual contracts to read and digest. If you opt out surveillance capitalists will threaten to downgrade your system and will probably still collect and distribute your information without your permission. You have no way to find out what they are doing. If you ask for the information collected, as a Belgium privacy attorney attempted to do of Google, they are unable to retrieve it for you. It is buried somewhere in a second tier of automatic computation technology. The user has no way of determining what software is currently running on your computers or smart phones or what peripherals like GPS, cameras, microphones, etc. have been usurped for external control. To add insult to injury, you will pay for the transmission bandwidth they secretly steal from you to illegally surveil your activities. If you have installed smart home devices like thermostats or security systems you have no way to know what these smart devices are observing and collecting. Your car driving behavior can be monitored with bad insurance consequences, not only by your new car, but by your smart phone. Your new car can be disabled by the finance company and its GPS location sent to the REPO people to come get your car. Then imagine advances in voice and face recognition and you start to get the terrifying idea. Then imagine all of this surveillance capability in the hands of a non democratic government like China. You can’t do anything at all without the state monitoring (and influencing) your behavior.

What does older capitalistic history teach us?

It (government interventions into free market capitalism) appeared in the trust busting, civil society, and legislative reforms of the Progressive Era. Later it was elaborated in the legislative, judicial, social, and tax initiatives of the New Deal and the institutionalization of Keynesian economic during the post-World War II era; labor market, tax, and social welfare policies that ultimately increased economic and social equality.

In fact the Bretton Woods conference of 1944 created a new world economic order based on a US-centric dollar based fixed exchange rate system, created the IMF and World Bank, and was a complete repudiation of Keynesian economics. This system worked only so long as the US remained the dominant manufacturing power, creating large trade surpluses that the US could recycle as investments. When trade reversed around 1970 and the US became a trade debtor nation, the American economy shifted from manufacture to financialization, convincing trade creditors to invest their surpluses with Wall Street, who kept inventing new and innovative ways to use the mountains of cash suddenly at their disposal. The Neoliberal contribution to all this was the erosion of government regulation of corporations and the use of IMF and Worldbank loans to vulnerable nations and colonies whose defaults resulted in the massive transfers of state owned commons into private hands like Wall Street hedge funds. See Greek Spring by Yanis Varoufakis. None of this history is clear from her book. For an excellent introduction to macro economics from Bretton Woods to the present see Yanis Varoufakis’ minotaur book. The breakup of the Soviet Union in the 1990’s was another opportunity for the Neoliberals who descended on the former Soviet Union members with plans to transfer all public commons into private hands. The result was to create a new class of asset owners in each country that more resembled a mafia than capitalists. We remain in this condition to this day. The massive and fundamental shift of the American economy from manufacture to financialization is not mentioned by Zuboff.

To her credit, Zuboff does site French economist Thomas Piketty’s monumental work on wealth and income distribution in England and America from the eighteenth century to the present.

A market economy…if left to itself…contains powerful forces of divergence, which are potentially threatening to democratic societies and to the values of social justice on which they are based…If we are to regain control of capital, we must bet everything on democracy.

Our present economic system has been accurately described as corporate welfare with massive government subsidies for agriculture, energy, extraction, and other industries. Hayek and Friedman would turn over in their graves if they knew where American capitalism has taken us. This trend reached its pinnacle (we only hope) with the Bush-Obama massive bailouts of the financial institutions and Zuboff’s beloved General Motors after the sub-prime financial scandal-crisis of 2008. Shiela Bair (W appointee to head the FDIC) was fully prepared to break up the big banks starting with Citibank using her FDIC authorization and charter, but was prevented from doing so by Tim Geithner who was shockingly appointed by Obama as his treasury secretary. See more at Scamming a President. No meaningful reforms were enacted to prevent a recurrence of this collapse and we anxiously await the next iteration.

Zuboff mentions Rand Corporation futurist Herman Kahn’s 1967 book The Year 2000, where the author anticipates the future possibilities of computer power intrusions into our lives characterizing this as “a twenty-first century nightmare”. She says Kahn was the model for the character of Dr. Strangelove in Stanley Kubrick’s 1964 movie. No!

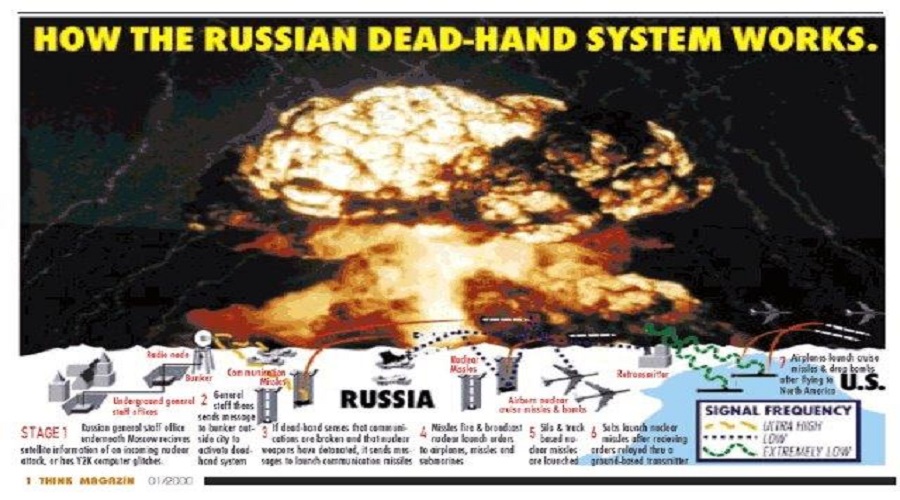

Herman Kahn wrote an earlier book published in 1960 “On Thermonuclear War” where Kahn speculated that it would be possible to create a “Doomsday Machine“; a vast collection of nuclear weapons connected to an automated trigger mechanism that, upon detection of a threat and without any human intervention, would initiate nuclear holocaust. Most experts at the time believed such a system could not be built. In fact the Soviet Union built just such a secret machine called The Dead Hand whose current status is unknown. See Daniel Ellsberg’s Doomsday Machine book. Kahn’s 1960 book was the inspiration for Kubrick’s movie where the Soviet Union have successfully built a doomsday machine but have kept it secret from the US. The character Dr. Strangelove is a caricature of a former Nazi scientist, not Kahn. Kahn was a consultant on the movie.

Zuboff uses a discussion of totalitarianism to illustrate how slow academics and intellectuals are to understand completely sui generis unprecedented developments. Our understanding of totalitarianism came into focus only in the 1960’s, well after the demise of European Fascism and dramatic changes following Stalin’s reign of terror. She points out that between 1930 and 1953 Stalin appears ten times on the cover of Time magazine. She leaves out any discussion of Mao’s China, but China emerges later in her discussion of State uses of surveillance capitalism.

She introduces and coins Instrumentarian power as a contrast to totalitarian power.

Instumentarian power moves differently and toward an opposite horizon. Totalitarianism operated through the means of violence, but intrumentarian power operates through the means of behavioral modification, and this is where our focus must shift. Intrumentarian power has no interest in our souls or any principal to instruct. There is no training or transformation for spiritual salvation, no ideology against which to judge our actions. It does not demand possession of each person from the inside out. It has no interest in exterminating or disfiguring our bodies and minds in the name of pure devotion. It welcomes data on the behavior of our blood and shit, but it has no interest in soiling itself with our excretions. It has no appetite for our grief, pain, or terror, although it eagerly welcomes the behavioral surplus that leaches from our anguish. It is profoundly and infinitely indifferent to our meanings and motives. Trained on measurable action, it only cares that whatever we do is accessible to its ever-evolving operations of rendition, calculation, modification, monetization, and control.

Deng Xiaoping Architect of Democracy Free Capitalism in China

Instrumentarian power in the hands of non democratic States like China is almost beyond comprehension in its potential power. Yanis Voroufakis describes Singapore under Lee Kuan Yew and his disciple Deng Xiaoping who transformed China’s economy using the Singapore model as democracy free capitalism.

Voroufakis primary point in Voroufakis Ted talk is that Western capitalist corporations are hording massive mountains of profit, investing only in corporate consolidation, and are in direct contradictions of Keynesian economics to recycle surpluses to level the cycles of boom and bust. These uninvested surplus mountains may doom democracy and life as we know it.

Industrial capitalism depended upon the exploitation and control of nature, with catastrophic consequences that we only now recognize. Surveillance capitalism…depends instead upon the exploitation and control of human nature. The market reduces us to our behavior, transformed into another fictional commodity and packaged for others’ consumption.

Surveillance capitalism’s successful claims to freedom and knowledge, its structural independence from people, its collectivist ambitions, and the radical indifference that is necessitated, enable, and sustained by all three now propel us toward a society in which capitalism does not function as a means to inclusive economic or political institutions. Instead, surveillance capitalism must be reckoned as a profoundly antidemocratic social force.

As Thomas Paine noted in the Eighteenth century; “…a body of men holding themselves accountable to nobody, ought not to be trusted by any body.”

Surveillance capitalism’s antidemocratic and anti egalitarian juggernaut is best described as a market-driven coup from above. It is not a coup d’etat in the classic sense but rather a coup de gens: an overthrow of the people concealed as a technological Trojan horse that is Big Other…It is a form of tyranny that feeds on people but is not of the people.

The young people we have considered…are the spirits of Christmas yet to come. They live on the frontier of a new form of power that declares the end of a human future, with its antique allegiances to individuals, democracy, and the human agency necessary for moral judgment. Should we awaken from distraction, resignation, and psychic numbing…it is a future that we may still avert.

Zuboff starts her book with the assertion that Surveillance capitalism cannot be controlled or contained through the lens of antitrust or privacy. She mentions the EU regulation the General Data Protection Regulation (GDPR) which only went into effect in May 2018 and only within the EU. It is too early to see if this ambitious effort will have any impact as it works its ways through EU regulators and the courts. She appears sceptical. For the Guardian’s take on GDPR. So what do we do?

If democracy is to be replenished in the coming decades, it is up to us to rekindle the sense of outrage and loss over what is being taken from us. In this I do not mean only our “personal information”. What is at stake here is the human expectation of sovereignty over one’s own life and authorship of one’s own experience. What is at stake is the inward experience from which we form the will to will and the public spaces to act on that will…That Surveillance capitalism has usurped so many of our rights in these domains is a scandalous abuse of digital capabilities and their once grand promise to democratize knowledge and meet our thwarted needs for effective life.

For more on the despotic behavior of Facebook and Google

Confidence Men, Wall Street, Washington, and the Education of a President, Ron Suskind 2011

The title is intended as a play on the word “confidence”, used to describe the primary motivations of Tim Geithner, Ben Bernanke and Larry Summers in dealing with the financial crisis as in “the proper role of government is to restore confidence in the financial institutions”. The second intended meaning of Suskind is how this small group of men manipulated, conned, scammed the President into following their policies and not the policies actually desired if not ordered by the President. Pretty strong stuff.

The book is a long rambling story telling of events from the long run for President, through the financial meltdown and the first years of the Presidency with an emphasis on the financial crisis but with excursions into health care reform and the auto bailout. It is so rambling that sometimes Suskind gets his facts mixed up as when he says health care insurers have revenues totaling $12 billion of the $2.5 trillion industry (page 193). Insurers profits alone exceed $12 billion! He sometimes loses the narrative as when he implies that Obama has already decided on an insurance mandate at the first health care summit where he gave the last word to insurance lobbyist Karen Ignagni. Then later in the book when health care reform again comes up for discussion it seems Obama has not decided on a mandate. And then Obama campaigned promising a public option. But here the problem may not be with the storyteller but with the man himself and this reader suggests this book is best seen as an imperfect study of the enigma that is our President.

After all, it doesn’t take a genius to figure out how these key players would act given their outsized egos, their personalities, and their history. Summers is a bully with highly toned rhetorical debating skills who is not embarrassed to dominate a discussion on subjects he knows nothing about. As Treasury Secretary in 1999 he was the moving force behind the Clinton administration dismantling of Glass-Steagall to allow Citibank to merge with Travelers Insurance bring Solomon and Smith Barney, two wall street investment banks into the Citi fold. He also made sure that the derivatives market would remain unregulated. These acts make Summers next only to Fed Chair Greenspan the most culpable enablers of the financial meltdown. It is equally revealing that Summers existed totally in the shadow of Bob Rubin so long as Rubin was Treasury Secretary for Clinton. Bullies know their place in the kicking order.

Geithner is a lifelong public servant who spend time in Washington and New York. At the New York Fed he was the shoe shine boy of wall street and the bankers who called him the “boy scout” behind his back. He and Bernanke together with former Goldman CEO ($750 million compensation) Hank Paulson engineered the bank rescue plan and further consolidation of finance as Wachovia, Washington Mutual, Bear Sterns, and Merill Lynch were swallowed up by the big banks. Geithner is not a public servant, he is a servant of Wall Street. It also turns out he is a tax cheat, failing to pay the IRS $34,000. Either he is cheating or he is incompetent, great choice! Incidentally, it seems Geithner’s father at the Ford foundation met Obama’s mother at least once in Indonesia. From Wikipedia;

From January 1981 to November 1984, Dunham (Barack’s mom) was the program officer for women and employment in the Ford Foundation’s Southeast Asia regional office in Jakarta. While at the Ford Foundation, she developed a model of microfinance which is now the standard in Indonesia, a country that is a world leader in micro-credit systems. Peter Geithner, father of Tim Geithner (who later became U.S. Secretary of the Treasury in her son’s administration), was head of the foundation’s Asia grant-making at that time.

Bernanke Lavishes free $14 Trillion on Wall Street

Ben Bernanke was touted as an expert on the Great Depression when he became Chairman of the Fed at the beginning of the meltdown. He was at all the merger and bailout meetings but we only now are learning the extent to which the Fed was secretly lending money to troubled institutions throughout the period. Recent Freedom of Information material acquired by Bloomberg is finally starting to shed some light on the extent of the exposure of the public in Fed lending to the banksters. The Fed has secretly loaned a peak of $1.2 Trillion to Wall Street and the banks including many European banks. Yes, public money has been loaned to European firms. That $1.2 trillion is the same total as all delinquent and foreclosed US home loans. Suskind put the figure at $3.5 trillion from 2007 to 2009. This brings the total Fed issuance to $14 trillion. If that money is used to purchase Treasuries at 3% this free money would yield the banks about $350 billion. So much for lessons on the Great Depression.

But the problem is not these characters who would be expected to act as they have. The important question is how did the President come to appoint them to positions where they could do more damage. Even Bernanke could have been replaced in 2009 when his first term ended.

President elect with Paul Volcker and Austan Goolsbee

Suskind characterized this question as Team A verses Team B. Team A, led by venerable Paul Volcker, was with Obama from the beginning of his candidacy and in-so-far as Obama’s superior knowledge of the workings and problems in the financial sector secured him election, it is thanks to Team A education and advice. On team A were Volcker, Austan Goolsbee, Robert Wolf (CEO of UBS and eyewitness of the meltdown meetings), Robert Reich, Stanley O’Neill, and William Donaldson. All expected significant rolls in the new administration, with Volcker as Treasury Secretary.

Obama Picks Team B

So how and why did Obama go with team B led by Geithner and Summers? We don’t have a clue. Byron Dorgan, Senator from North Dakota put it most eloquently; “You’ve picked the wrong people…I don’t understand how you could do this. You’ve picked the wrong people.” We voters all felt the same way. Where’s our change?

Daschle Master of Congress Left Behind

But Obama was not done yet. He needed to choose between longtime master of the senate, the low key, soft spoken, extremely tough Tom Daschle, and the brash, volatile, inexperienced, caustic, egotistical fourth ranked representative Rahm Emmanuel for his Chief of Staff, doorkeeper to the President. Tough choice right? We’ll go with the much hated in Congress Rahm. What is this man doing to himself? And even worse, Obama spent so much political capital getting Geithner appointed despite his personal tax problems that Obama loses entirely the services of Dacshle, who has a minor problem in failing to report the use of a lobbyist provide car while in Washington. Dacshle could have been confirmed before Geithner but not after. So Obama trades Dacshle for Geithner.

During this transition period, Obama is reading up on FDR who in his first hundred day in office passed the Emergency banking and Glass-Steagall acts, establishes the FDIC to insure deposits, created the Civilian Conservation Corps and the Tennessee Valley Authority. He passed the Farm Credit, Truth in Securities, and the National Recovery Acts, and others. The basis of the entire New Deal were in place within 100 days of FDR assuming office. While detractors point out that full recovery did not happen until WWII started, there was never doubt in Americans minds that the country was back on track early in 1933. Obama assumed office with no plans whatever; none; nada! So much for the legacy of FDR. And he appoints a team guaranteed to continue undermining the FDR legacy.

Two million people showed up in the freezing cold to watch the Obama inauguration and hope. Elizabeth Warren first met Obama at a campaign event in Chicago. Afterward Obama talked about being inside the bubble; “I haven’t been living in this bubble very long. I’m in it now, but not that long ago I had a real life.”

“And she (Warren) would wonder, replaying that last conversation in her head, if it was really about the bubble or the character of the man inside the bubble, and if in Chicago she had seem what she hoped to see, rather than what was really there.”

There are a lot of us wondering this same thing now.

Elizabeth Warren will not head Consumer Financial Protection Bureau

See Warren As TARP Oversight Chair Take on Geithner

You can’t run a policy based on a misdirection or a fiction. I don’t know what the president is thinking. I don’t see the president. He meets with bankers. He doesn’t meet with me. But if he’s involved in this at all, he’s got to know that his angry words at Wall Street, and their recklessness and dangerous incentives in compensation, about how they do their business in ways utterly divorced from what’s actually good for the economy – that he can’t just say that sort of thing and then just dump money in their laps and be credible. Tim and Larry’s whole plan is just like Argentina’s in the 1980s. There was this giant hole marked “Banks” and the government just dumped money in that hole, as much as they had, while they lied about it. That’s what Larry thinks, that the U.S. is Argentina.”

Elizabeth Warren, who was the driving force in establishing the Consumer Financial Protection Bureau to which Obama failed to make its first head and which was crippled at its inception by placing it in the Federal Reserve – toothless. This leads Suskind to another startling theme that links Obama, Summers, Emmanuel, and Geithner, their seeming inability to deal with women professional as equals. Suskind suggests that Summers was fired from the Presidency of Harvard not only because he suggested that women were genetically unsuited to science, but because during his tenure only four women were promoted at Harvard. Hillary, as a world recognized force of nature is the sole exception, viewed not as a woman, but as a power base. Suskind suggests that Christina Romer was given a “safe” ie. non threatening to Geithner and Summers appointment in a nod to gender equality.